Analyse the Effects of Digital Currencies on Traditional Financial Systems

Analyse the Effects of Digital Currencies on Traditional Financial Systems

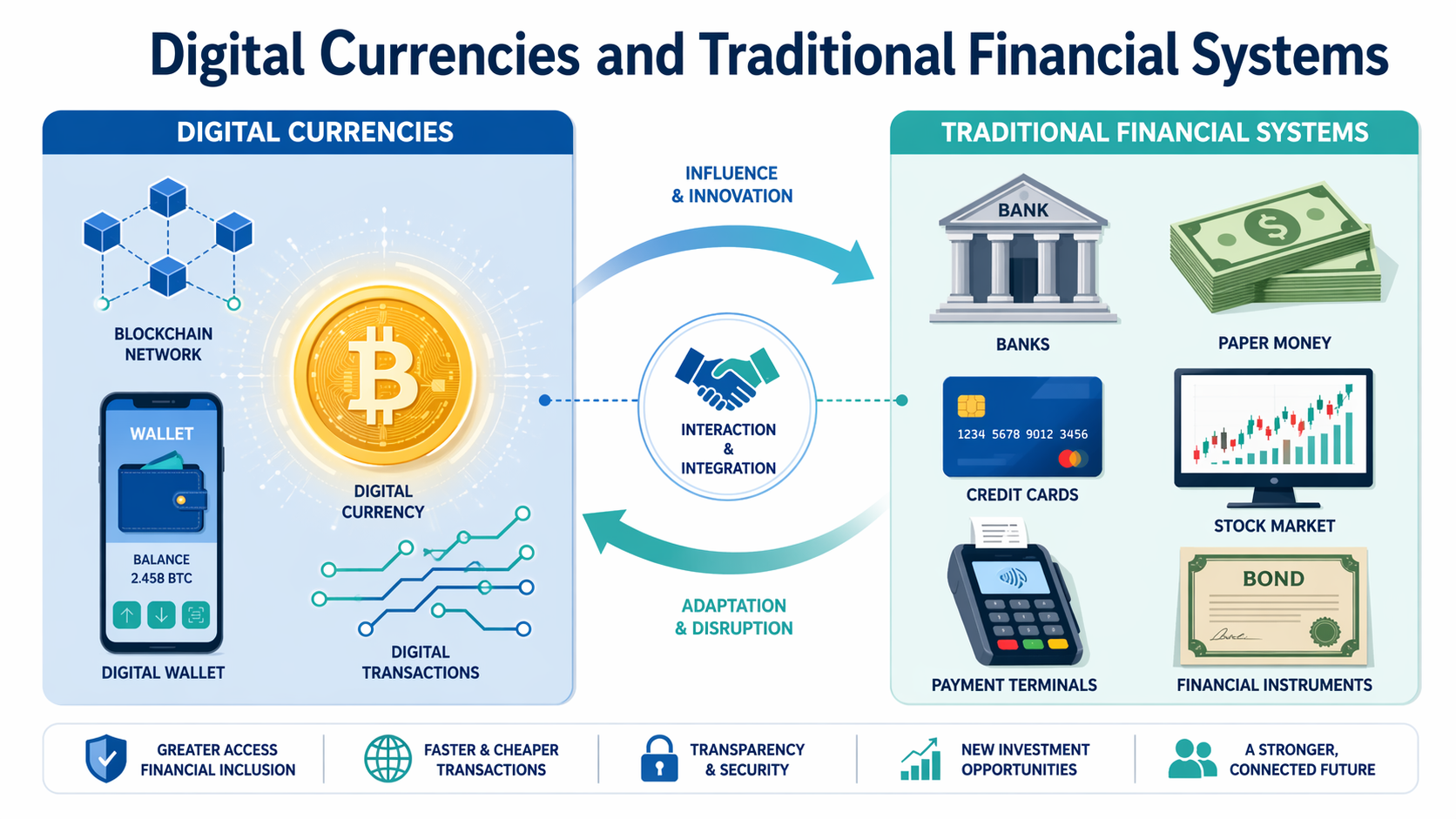

If money is a language, digital currencies are the slang teenagers pick up first and central banks rush to learn later. “Digital currency” is not one thing. It has two families: public money in a new wrapper, such as the Reserve Bank of India’s central bank digital currency, the e₹, and private crypto such as Bitcoin, Ethereum, and rupee-pegged stablecoins. Together, they pressure the old financial system on speed, cost, and what money can do. India is the perfect lab because it already runs on an instant-pay rail at massive scale: UPI processed around 20.0 billion transactions in August 2025 (NPCI, 2025).

Digital Rupee and the Existing Financial System

The RBI’s retail e₹ pilot has been live since December 2022. The digital rupee is issued by the central bank, designed to be cash-like, and is exploring offline payments and programmability (RBI, 2025). This is digital money, while UPI is a payment system. The e₹ can sit alongside UPI rather than replace it (RBI, 2025).

For a teenager, this means you will still tap UPI for metro rides or split a pizza because it is ubiquitous and merchant-friendly (NPCI, 2025). Legally, minors above 10 may operate savings accounts independently, subject to bank-set limits, so teens already live comfortably in the UPI universe (RBI, 2014). But most Indian crypto exchanges are 18+ because onboarding is tied to KYC and AML rules (WazirX, 2024). So crypto is largely a parent-supervised experiment until adulthood, while e₹ access is arriving through the same banks that already power teens’ UPI lives (RBI, 2025).

Effects on Banks and Payment Companies

Systemically, digital currencies push banks and payments companies to improve. If households begin holding more value in an e₹ wallet, which is a direct RBI liability, instead of bank deposits, banks could feel some pressure on their funding. That is why most CBDC designs lean toward being non-interest-bearing and having holding limits, to reduce the risk of banks losing deposits too quickly (IMF, 2024).

At the same time, programmability hints at a new kind of public-finance infrastructure. Governments could use digital rupee systems for attendance-linked stipends, targeted scholarships, or subsidies that settle instantly and leave clear audit trails. These ideas are being explored in CBDC pilots, even if they are not yet used at large scale (RBI, 2025).

Private Crypto and Regulatory Pressure

The hard questions are about safety, regulation, and long-term viability. India’s stance toward private crypto remains cautious. Since Budget 2022, gains from transferring virtual digital assets have been taxed at 30%, and a 1% TDS applies above certain thresholds. These rules do not ban crypto, but they fence it off and make casual speculation more expensive and traceable (GoI Income-tax Department, 2022a; 2022b).

Separately, since March 2023, service providers have been treated as reporting entities, which tightens KYC and AML compliance. FIU-IND has also taken enforcement actions against non-compliant offshore platforms (PIB / FIU-IND, 2025). For teenagers, the message is simple: if you ever interact with crypto through a parent or guardian, treat it like investing in a volatile foreign language, where mistakes can be costly.

Risks and Consumer Protection

There is also operational risk. On public blockchains, transactions are irreversible. There are no chargebacks if you paste the wrong wallet address or fall for a scam (Bitcoin.org). Phishing, fake airdrops, and too-good-to-be-true mentors often target beginners. Custody is also a trade-off: you can control your own seed phrase and risk losing it, or use a custodian and trust someone else to protect your assets.

Privacy is another issue. RBI frames e₹ as cash-like, but true privacy depends on policy choices and wallet design. Current pilots are exploring thresholds, offline modes, and selective programmability. UPI, by contrast, is tightly linked to KYC-verified bank accounts (RBI, 2025).

Conclusion

In India, digital currencies are unlikely to blow up the traditional financial system. Instead, they are forcing it to modernize. Banks, payment companies, and regulators now have to respond to faster settlement, lower friction, greater transparency, and new expectations around how money should move. For teenagers, the smartest path right now is still UPI plus strong financial literacy, while e₹ arrives gradually as a mix of civics, technology, and finance in everyday life.

References

Bidder, R., Jackson, T. and Rottner, M. (2025) CBDC and banks: Disintermediating fast and slow. Bank for International Settlements Working Paper No. 1280.

Bitcoin.org (n.d.) Some things you need to know.

CERT-In (2024) Advisory on cryptocurrency scams and phishing tactics.

CoinDCX (2022) Okto / CoinDCX Terms of Service.

GoI Income-tax Department (2022a) Section 115BBH—Tax on income from virtual digital assets.

GoI Income-tax Department (2022b) Section 194S—TDS on transfer of virtual digital assets.

IMF (2024) Central Bank Digital Currencies and Financial Stability.

NPCI (2025) UPI Product Statistics (Monthly Metrics).

PIB / FIU-IND (2023) FIU-IND issues show-cause notices to offshore VDA SPs; VDAs brought under PMLA in March 2023.

PIB / FIU-IND (2025) FIU-IND imposes monetary penalty on Bybit for PMLA violations.

RBI (2014) Opening of bank accounts in the names of minors—Guidelines.

RBI (2025) Digital Rupee (e₹) – FAQs.

WazirX (2024) Terms of Use.

Investopedia (n.d.) Blockchain facts / Irreversibility of on-chain transactions.

NPCI (2025) UPI overview—Bank-to-bank, KYC-linked real-time payments.